Kansas K 19 PDF Form

Kansas K 19 PDF Form

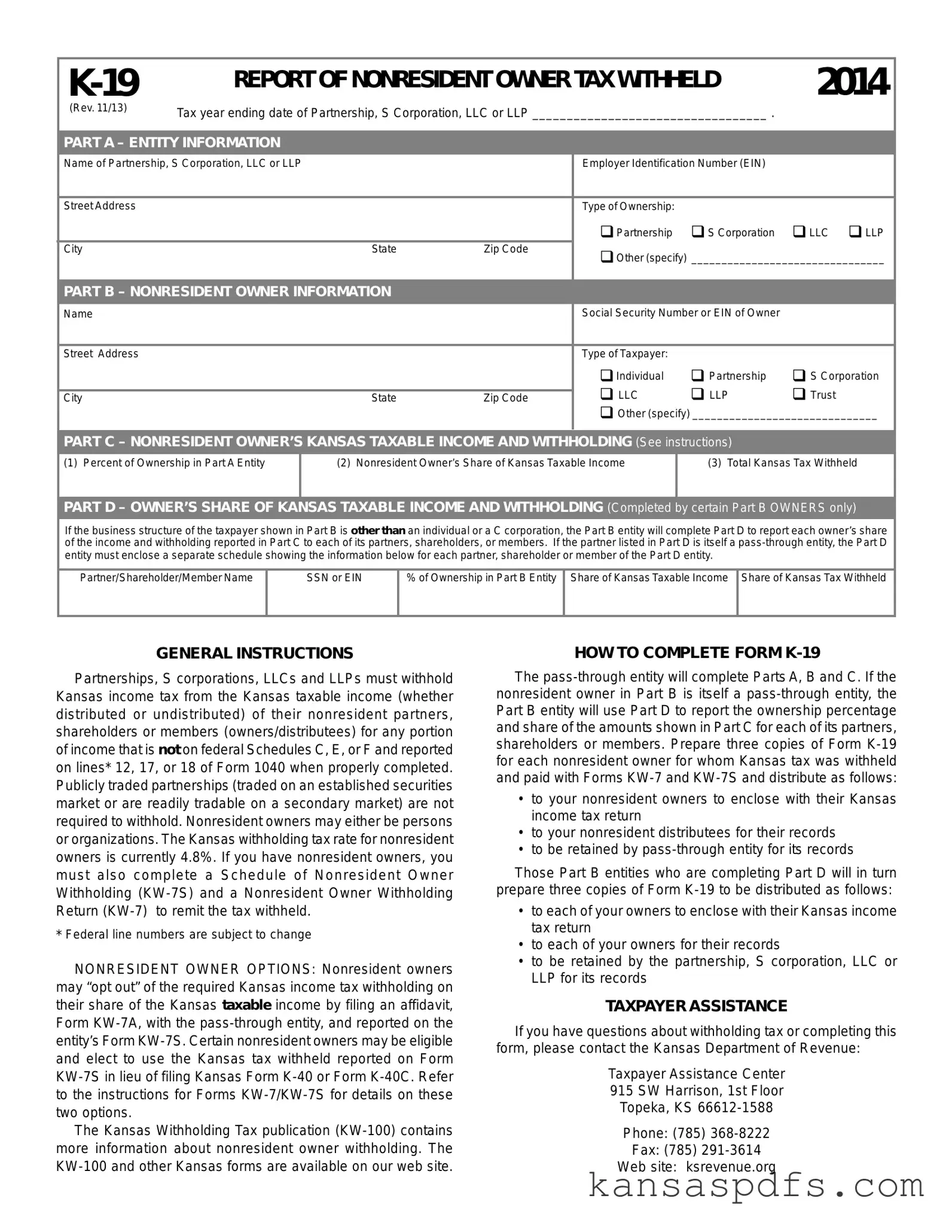

Understanding the intricacies of tax obligations can be daunting, especially when dealing with the specifics of nonresident owner tax withholding in Kansas. The K-19 Report of Nonresident Owner Tax Withheld plays a critical role in this process. Designed for use by partnerships, S corporations, LLCs, and LLPs, this form ensures that Kansas income tax is properly withheld from the Kansas taxable income attributed to their nonresident partners, shareholders, or members. It encompasses detailed sections for entity information, nonresident owner details, the owner’s share of Kansas taxable income and the tax withheld. Furthermore, it addresses the distribution of this information through a meticulous reporting structure should the nonresident owner be another pass-through entity. Entities are obliged to withhold income tax at a standard rate of 4.9%, despite the option available for nonresident owners to opt out under specific conditions, by filing an affidavit. Additionally, the form meticulously outlines the eligibility for certain nonresident owners to utilize the Kansas tax withheld in lieu of filing separate Kansas income tax returns. This form not only facilitates compliance with state tax laws but also streamlines the process for both entities and their nonresident owners, ensuring the correct allocation and reporting of withheld taxes

REPORT OF NONRESIDENT OWNER TAX WITHHELD |

2014 |

||||

(Rev. 11/13) |

Tax year ending date of Partnership, S Corporation, LLC or LLP __________________________________ . |

|

|||

|

|

||||

|

|

|

|

|

|

PART A – ENTITY INFORMATION |

|

|

|

|

|

Name of Partnership, S Corporation, LLC or LLP |

|

Employer Identification Number (EIN) |

|

||

|

|

|

|

|

|

Street Address |

|

|

Type of Ownership: |

|

|

|

|

|

Partnership |

S Corporation |

LLC LLP |

City |

State |

Zip Code |

Other (specify) ________________________________ |

||

|

|

|

|||

|

|

|

|

|

|

PART B – NONRESIDENT OWNER INFORMATION |

|

|

|

|

|

Name |

|

|

Social Security Number or EIN of Owner |

|

|

|

|

|

|

|

|

Street Address |

|

|

Type of Taxpayer: |

|

|

|

|

|

Individual |

Partnership |

S Corporation |

|

|

|

LLC |

LLP |

Trust |

City |

State |

Zip Code |

|||

|

|

|

Other (specify) ______________________________ |

||

|

|

|

|

|

|

PART C – NONRESIDENT OWNER’S KANSAS TAXABLE INCOME AND WITHHOLDING (See instructions)

(1) Percent of Ownership in Part A Entity

(2) Nonresident Owner’s Share of Kansas Taxable Income

(3) Total Kansas Tax Withheld

PART D – OWNER’S SHARE OF KANSAS TAXABLE INCOME AND WITHHOLDING (Completed by certain Part B OWNERS only)

If the business structure of the taxpayer shown in Part B is other than an individual or a C corporation, the Part B entity will complete Part D to report each owner’s share of the income and withholding reported in Part C to each of its partners, shareholders, or members. If the partner listed in Part D is itself a

Partner/Shareholder/Member Name

SSN or EIN

% of Ownership in Part B Entity

Share of Kansas Taxable Income

Share of Kansas Tax Withheld

GENERAL INSTRUCTIONS

Partnerships, S corporations, LLCs and LLPs must withhold Kansas income tax from the Kansas taxable income (whether distributed or undistributed) of their nonresident partners, shareholders or members (owners/distributees) for any portion of income that is not on federal Schedules C, E, or F and reported on lines* 12, 17, or 18 of Form 1040 when properly completed. Publicly traded partnerships (traded on an established securities market or are readily tradable on a secondary market) are not required to withhold. Nonresident owners may either be persons or organizations. The Kansas withholding tax rate for nonresident owners is currently 4.8%. If you have nonresident owners, you must also complete a Schedule of Nonresident Owner Withholding

*Federal line numbers are subject to change

NONRESIDENT OWNER OPTIONS: Nonresident owners may “opt out” of the required Kansas income tax withholding on their share of the Kansas taxable income by filing an affidavit, Form

The Kansas Withholding Tax publication

HOW TO COMPLETE FORM

The

•to your nonresident owners to enclose with their Kansas income tax return

•to your nonresident distributees for their records

•to be retained by

Those Part B entities who are completing Part D will in turn prepare three copies of Form

•to each of your owners to enclose with their Kansas income tax return

•to each of your owners for their records

•to be retained by the partnership, S corporation, LLC or LLP for its records

TAXPAYER ASSISTANCE

If you have questions about withholding tax or completing this form, please contact the Kansas Department of Revenue:

Taxpayer Assistance Center

915 SW Harrison, 1st Floor

Topeka, KS

Phone: (785)

Fax: (785)

Web site: ksrevenue.org

| Fact | Detail |

|---|---|

| Form Name | K-19 REPORT OF NONRESIDENT OWNER TAX WITHHELD |

| Revision Date | November 2013 |

| Applicability | Pass-through entities like Partnerships, S Corporations, LLCs, or LLPs |

| Purpose | To report Kansas income tax withheld from nonresident owners' shares |

| Governing Law | Kansas State Tax Laws |

| Withholding Tax Rate | Currently 4.9% |

| Exemptions | Publicly traded partnerships are not required to withhold |

| Options for Nonresident Owners | May opt out of withholding or elect to use withheld amount differently |

| Affiliated Forms | KW-7, KW-7S, and potentially KW-7A for opt-out affidavit |

| Filing Requirement | Three copies per nonresident owner: one for filing, one for their records, one for the entity's records |

| Taxpayer Assistance | Kansas Department of Revenue offers assistance via phone, fax, and online |

Filling out the Kansas K-19 form is a crucial step for partnerships, S corporations, LLCs, and LLPs that have nonresident owners and are subject to income tax withholding requirements in Kansas. This procedure ensures compliance with state tax obligations by accurately reporting the income and withholding tax for nonresident owners. The process might appear daunting at first, but breaking it down into straightforward steps will simplify filling out the form accurately and efficiently. It is essential for the entity to complete this form meticulously to avoid potential errors that could lead to penalties or delays.

After completing the form and making the necessary copies, the next steps involve compliance with Kansas tax withholding and reporting requirements. It’s important to remember that entities must also complete the Schedule of Nonresident Owner Withholding (KW-7S) and the Nonresident Owner Withholding Return (KW-7) to remit the tax withheld. These steps ensure that both the entity and the nonresident owners meet their tax obligations under Kansas law. Always refer to the latest instructions and guidelines provided by the Kansas Department of Revenue to stay compliant and avoid any potential mistakes in the process.

What is the Kansas K-19 form?

The Kansas K-19 form, commonly known as the "Report of Nonresident Owner Tax Withheld," is a document used by partnerships, S corporations, LLCs, and LLPs to report income tax withheld for nonresident owners. This form details the nonresident owner's share of Kansas taxable income and the corresponding tax withheld.

Who needs to file the Kansas K-19 form?

Partnerships, S corporations, LLCs, and LLPs that have nonresident partners, shareholders, or members (owners/distributees) must file the K-19 form. This requirement applies if the owners' share of income is not reported on federal Schedules C, E, or F.

What information is required on the K-19 form?

The form requires entity information (Part A), nonresident owner information (Part B), the nonresident owner’s share of Kansas taxable income and withholding (Part C), and if applicable, each owner’s share of income and withholding if the owner in Part B is a pass-through entity (Part D).

How does a nonresident owner "opt-out" of Kansas income tax withholding?

Nonresident owners may opt out of Kansas income tax withholding by filing an affidavit, Form KW-7A, with the pass-through entity. This affidavit should then be reported on the entity’s Form KW-7S.

Are there any exemptions to the withholding requirement?

Yes, publicly traded partnerships that are traded on an established securities market or are readily tradable on a secondary market are not required to withhold Kansas income tax for their nonresident owners.

What should be done with the completed K-19 forms?

Three copies of the completed K-19 form should be prepared for each nonresident owner: one to be enclosed with their Kansas income tax return, one for the nonresident owner's records, and one to be retained by the pass-through entity. If Part D is completed, similarly distribute the forms among the respective owners and entities involved.

How does the withholding tax rate currently stand for nonresident owners in Kansas?

The current Kansas withholding tax rate for nonresident owners is 4.9%.

Where can more information about nonresident owner withholding be found?

More detailed information about nonresident owner withholding can be found in the Kansas Withholding Tax publication (KW-100) and other forms, which are available on the Kansas Department of Revenue website.

When filling out the Kansas K-19 form, Report of Nonresident Owner Tax Withheld, people often make errors that can delay processing or result in incorrect withholding amounts. Attention to detail is crucial to avoid these common mistakes:

To ensure accuracy and compliance, it is important for individuals completing the Kansas K-19 form to read all instructions carefully, verify all provided information, and confirm that all required attachments and copies are accurately prepared and properly distributed.

When dealing with Kansas tax matters, particularly for nonresident owners, you're likely to encounter more than just the K-19 form. Each form serves its unique purpose in the framework of tax documentation and compliance. Familiarity with these forms ensures a more comprehensive approach to handling tax responsibilities.

Combining thorough documentation with an understanding of each form’s role simplifies the complexity of tax compliance, ensuring that all legal obligations are met efficiently. Ensuring that you have all the necessary forms ready goes a long way in streamlining the filing process, making tax season smoother for both the entity and its nonresident owners.

The Kansas K-19 form, known as the "Report of Nonresident Owner Tax Withheld," is similar to several other tax forms used across the United States for reporting and withholding tax purposes. This document is specifically tailored for partnerships, S corporations, LLCs, or LLPs that need to report income and tax withholdings for their nonresident owners. Similar forms in other contexts include the IRS Form 1042 and the Form 8805. Each of these forms serves a unique purpose but shares common elements in reporting nonresident income and withholding tax.

First among the comparable documents is the IRS Form 1042, "Annual Withholding Tax Return for U.S. Source Income of Foreign Persons." Like the Kansas K-19, Form 1042 is used to report tax withheld on certain income associated with nonresident entities. However, Form 1042 focuses on income considered to be from U.S. sources paid to foreign persons or entities, capturing a broader range of nonresident withholding beyond the state level. Despite their different scopes – one being federal and the other state-specific – both forms ensure compliance with tax obligations for nonresident income earners.

Similarly, the Form 8805, "Foreign Partner's Information Statement of Section 1446 Withholding Tax," parallels the Kansas K-19 in its requirement for partnerships to report and withhold income tax on earnings distributed to foreign partners. Form 8805 is specifically used to report withholdings under Section 1446 of the Internal Revenue Code, which involves partnerships generating income effectively connected with a U.S. trade or business and distributing this income to foreign partners. Like the K-19, it mandates the reporting entity to disclose the partner’s share of income and the corresponding amount of tax withheld. Both forms serve to inform the nonresident entities of their income and tax liabilities within the United States, ensuring proper compliance with tax laws.

When filling out the Kansas K-19 form, it's important to follow best practices to ensure the accuracy and compliance of the submission. Below are key dos and don’ts to consider:

Do:

Don't:

There are common misconceptions about the Kansas K-19 form, which is officially known as the REPORT OF NONRESIDENT OWNER TAX WITHHELD. Understanding the purpose and requirements of this form is crucial for entities and nonresident owners alike.

Misconception 1: The K-19 form applies to all businesses in Kansas. In reality, the K-19 form is specifically designed for pass-through entities, such as partnerships, S corporations, LLCs, and LLPs, that have nonresident owners. It is not required for C corporations or businesses without nonresident owners.

Misconception 2: All nonresident owners must have Kansas tax withheld. While Kansas law requires the withholding of income tax on the share of Kansas taxable income attributable to nonresident owners, there are exceptions. Nonresident owners can opt out of withholding by filing an affidavit (Form KW-7A) with the pass-through entity. Additionally, certain nonresident owners may not be subject to withholding based on specific criteria outlined by Kansas regulations.

Misconception 3: The K-19 form serves as the tax return for nonresident owners. This is incorrect. The K-19 form is a report of tax withheld by the pass-through entity and is used by nonresident owners to support the Kansas tax withheld when they file their own Kansas income tax returns. Nonresident owners must still file their individual Kansas income tax return, such as Form K-40 or K-40C, to report their share of income from Kansas sources.

Misconception 4: Withholding at the entity level eliminates the need for nonresident owners to file Kansas tax returns. The withholding is a prepayment of the tax due on income earned in Kansas. Nonresident owners must file a Kansas tax return to reconcile the total tax liability with the amount withheld and paid on their behalf by the pass-through entity. This could result in a refund or additional tax due.

It's important for entities and nonresident owners to understand these aspects of the K-19 form to ensure compliance with Kansas tax law and avoid potential issues. For specific guidance or assistance, contacting the Kansas Department of Revenue or a tax professional is recommended.

Filling out and using the Kansas K-19 form, formally known as the Report of Nonresident Owner Tax Withheld, comes with key considerations for partnerships, S corporations, LLCs, and LLPs. Below are crucial takeaways to ensure compliance and proper tax handling for nonresident owners:

Properly managing and understanding the intricacies of the K-19 form is essential for entities with nonresident owners in Kansas. By focusing on these key aspects, entities can navigate the complexities of state tax withholding requirements and maintain good standing with the Kansas Department of Revenue.

Tr-42 - Aids in preventing titling errors and delays when vehicles with Kansas liens are registered in new states.

Proof of Residency Kansas - Aids in the prompt and accurate verification of essential documents for Kansas residents navigating citizenship or residency verification.