Kansas K 30 PDF Form

Kansas K 30 PDF Form

The Kansas K-30 form plays a crucial role for angel investors in the state of Kansas, offering a significant tax credit incentive for investments in qualified Kansas businesses. Enacted to stimulate economic growth and innovation within the state, this form enables individuals and entities to claim a tax credit against their income or premium tax for cash investments made into businesses that meet certain criteria. The credit amounts to 50% of the investment made, with a cap of $50,000 per business and a total of $250,000 in tax credits per investor each year. However, it's important to note that the total tax credits available statewide are limited annually, with specific caps set for each tax year. For investments to qualify, the beneficiary business must first be approved by the Kansas Technology Enterprise Corporation (KTEC). Furthermore, the legislation outlines a carryforward provision for unused credits, permitting investors to apply these to their tax liabilities in subsequent years. Besides the credit's direct financial benefits, there are restrictions to be aware of, such as the prohibition on credits for investments in certain types of businesses and the exclusion of Kansas venture capital companies from eligibility. The angel investor tax credit also accommodates for the eventual transfer of the credit under specific conditions, extending flexibility to investors. Keeping accurate records, including the KTEC certification form, is essential for compliance and verification purposes. The administration and potential complexities of the Kansas K-30 form underscore the need for careful navigation to maximize benefits while adhering to regulatory requirements.

KANSAS |

|

|

||

|

(Rev. 8/11) |

ANGEL INVESTOR CREDIT |

||

|

|

|

|

|

|

|

For the taxable year beginning, _________________ , 20____ ; |

ending _________________ , 20____ . |

|

|

|

|

|

|

|

Name of taxpayer (as shown on return) |

|

Social Security Number |

|

|

|

|

|

|

|

If partner, shareholder or member, enter name of partnership, S corporation, LLC or LLP |

|

Employer ID Number (EIN) |

|

|

|

|

|

|

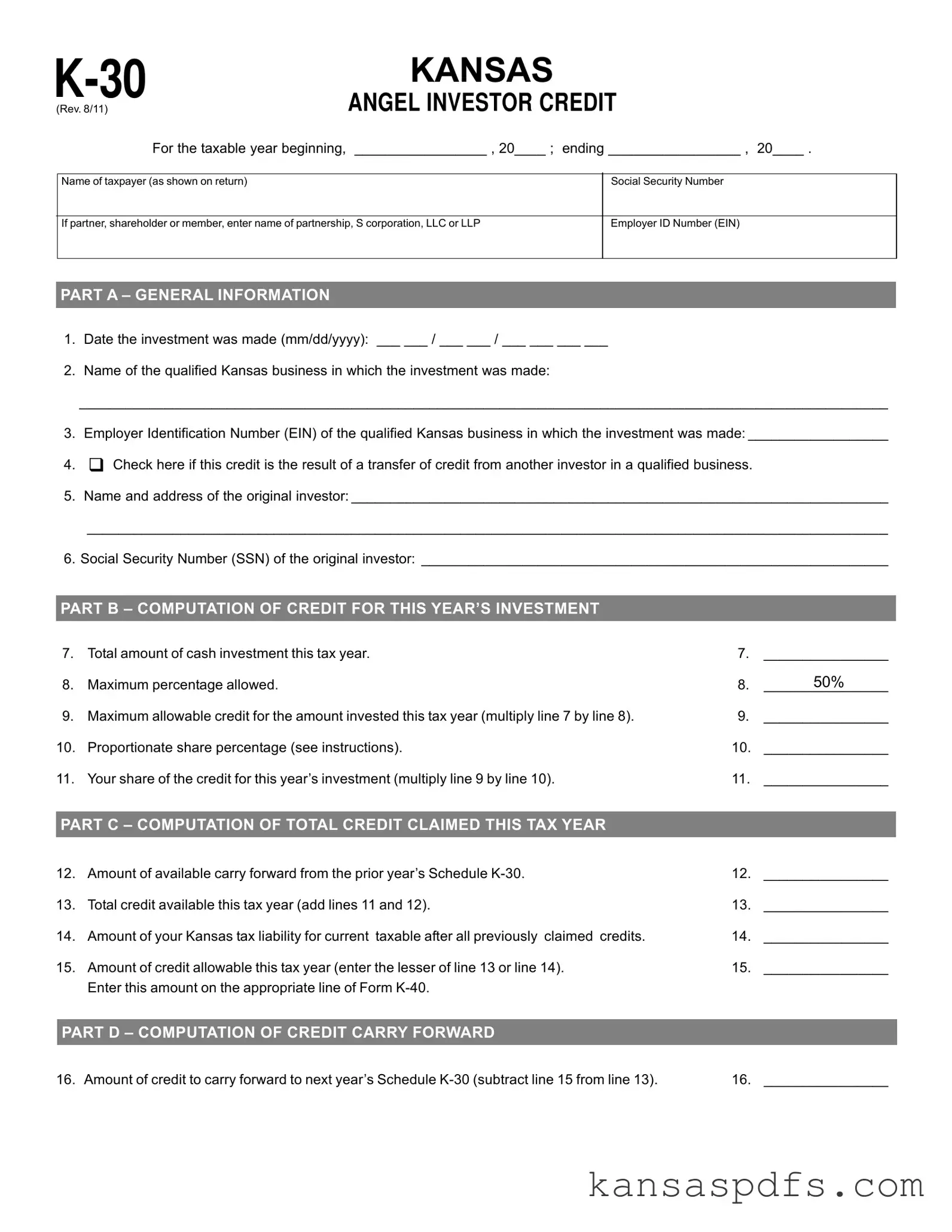

PART A – GENERAL INFORMATION

1.Date the investment was made (mm/dd/yyyy): ___ ___ / ___ ___ / ___ ___ ___ ___

2.Name of the qualified Kansas business in which the investment was made:

________________________________________________________________________________________________________

3.Employer Identification Number (EIN) of the qualified Kansas business in which the investment was made: __________________

4.ノ Check here if this credit is the result of a transfer of credit from another investor in a qualified business.

5.Name and address of the original investor: _____________________________________________________________________

_______________________________________________________________________________________________________

6.Social Security Number (SSN) of the original investor: ____________________________________________________________

PART B – COMPUTATION OF CREDIT FOR THIS YEAR’S INVESTMENT

7. Total amount of cash investment this tax year.7. ________________

8. |

Maximum percentage allowed. |

8. |

50% |

________________ |

|||

9. |

Maximum allowable credit for the amount invested this tax year (multiply line 7 by line 8). |

9. |

________________ |

10. |

Proportionate share percentage (see instructions). |

10. |

________________ |

11. |

Your share of the credit for this year’s investment (multiply line 9 by line 10). |

11. |

________________ |

|

|

|

|

PART C – COMPUTATION OF TOTAL CREDIT CLAIMED THIS TAX YEAR |

|

|

|

12. |

Amount of available carry forward from the prior year’s Schedule |

12. |

________________ |

13. |

Total credit available this tax year (add lines 11 and 12). |

13. |

________________ |

14. |

Amount of your Kansas tax liability for current taxable after all previously claimed credits. |

14. |

________________ |

15. |

Amount of credit allowable this tax year (enter the lesser of line 13 or line 14). |

15. |

________________ |

|

Enter this amount on the appropriate line of Form |

|

|

PART D – COMPUTATION OF CREDIT CARRY FORWARD

16. Amount of credit to carry forward to next year’s Schedule |

16. ________________ |

INSTRUCTIONS FOR SCHEDULE

|

GENERAL INSTRUCTIONS |

SPECIFIC LINE INSTRUCTIONS |

||

K.S.A. |

|

|||

PART A |

|

|||

premium tax of any angel investor for a cash investment in the |

LINES 1 through 6 – Complete the information for the qualified |

|||

qualified securities of a qualified Kansas business. |

||||

Kansas business and original investor as requested. |

||||

Before an angel investor may be entitled to receive tax credits, |

||||

|

|

|||

such investor must have made a cash investment in a qualified |

PART B |

|

||

security of a qualified Kansas business. The investment must be |

LINE 7 – Enter total amount of cash investment made this tax year. |

|||

made in a business that has been approved by KTEC (Kansas |

||||

LINE 8 – This percentage determines the maximum credit allowable |

||||

Technology Enterprise Corporation) as a qualified business prior |

||||

as a result of the investment made during this tax year. Do not |

||||

to the date on which the cash investment is made. For information |

||||

make an entry on this line. |

||||

and assistance regarding the approval of a qualified Kansas |

||||

LINE 9 – Multiply line 7 by line 8 and enter the result. This is the |

||||

business, contact KTEC at (785) |

||||

maximum credit allowable. |

||||

The credit is 50% of such investors’ cash investment in any |

||||

LINE 10 – Partners, shareholders or members: Enter the percentage |

||||

qualified Kansas business, subject to the following limitations: |

||||

that represents your proportionate share in the partnership, S |

||||

|

|

|||

• No tax credits will be allowed for more than $50,000 for a single |

corporation, LLC or LLP. All other taxpayers: Enter 100%. |

|||

|

Kansasbusinessoratotalof$250,000intaxcreditsforasingle |

LINE 11 – Multiply line 9 by line 10 and enter result. This is your |

||

|

year per investor who is a natural person or owner of a |

share of the total credit for the amount invested this year. |

||

|

permitted entity investor. |

|

|

|

|

PART C |

|

||

• No tax credits shall be allowed for any cash investments in |

|

|||

LINE 12 – Enter the carry forward amounts available from prior |

||||

|

qualified securities for any year after the year 2016. |

|||

• |

The total amount of tax credits shall not exceed $6,000,000 |

years’ |

||

2010 legislation (SB 430) allows taxpayers that had credits |

||||

|

for tax year 2008 and each tax year thereafter, except that for |

|||

|

earned pursuant to K.S.A. |

|||

|

tax year 2011, the total amount of tax credits shall not exceed |

|||

|

year 2011 any reduction that occurred in tax year 2009 |

|||

|

$5,000,000. |

|||

|

and/or 2010. Enter those amounts here on line 12. |

|||

• |

No investor shall claim a credit for cash investments in Kansas |

|||

LINE 13 – Add lines 11 & 12 and enter the result. |

||||

|

Venture Capital, Inc. |

|||

|

LINE 14 – Enter your total Kansas tax liability for the current tax |

|||

• |

No Kansas venture capital company shall qualify for the tax |

|||

year after all credits other than the credit allowed for |

||||

|

credit for an investment in a fund created by articles 81, 82, |

|||

|

investments made during this tax year. |

|||

|

83 or 84 of chapter 74 of the Kansas Statutes Annotated. |

|||

|

LINE 15 – Enter the lesser of line 13 or line 14. Enter this amount |

|||

If the amount by which that portion of the credit allowed by this |

||||

on the appropriate line of Form |

||||

section exceeds the investors’ liability in any one taxable year, the |

||||

|

|

|||

PART D |

|

|||

remaining portion of the credit may be carried forward until the total |

|

|||

|

|

|||

amount of the credit is used. If the investor is a permitted entity |

LINE 16 – Subtract line 15 from line 13 and enter result. This |

|||

investor, the credit provided by this section shall be claimed by the |

||||

amount cannot be less than zero. Enter this amount on next |

||||

owners of the permitted entity investor in proportion to their |

||||

year’s Schedule |

||||

|

|

|||

ownership share of the permitted entity investor. |

|

|

||

Subject to certain restrictions this credit may be transferred to |

IMPORTANT: Do not send any enclosures with this |

|||

schedule. A copy of the approved KTEC certification |

||||

another taxpayer. Contact KTEC at (785) |

||||

form must be kept with your records. If this is a credit |

||||

information. |

||||

that has been transferred, documentation of the approved transfer |

||||

|

|

|||

“Angel investor’’and ‘‘investor’’meanYXWVUTSRan accredited investor |

||||

|

|

as provided by KDOR (Kansas Department of Revenue) must be |

||

who is a natural person or an owner of a permitted entity investor, |

retained with your records. KDOR reserves the right to request |

|||

who is of high net worth, as defined in 17 C.F.R. 230.501(a) as in |

additional information as necessary. |

|||

effect on the effective date of this act, and who seeks high returns |

|

|

||

through private investments in |

TAXPAYERASSISTANCE |

|||

active involvement in business, such as consulting and mentoring |

For assistance in completing this schedule contact the Kansas |

|||

the entrepreneur. |

||||

Department of Revenue: |

||||

“Cash investment” means money or money equivalent in |

||||

Tax Operations |

||||

consideration for qualified securities. |

||||

Docking State Office Building, 1st fl. |

||||

“Permittedentityinvestor”means any: a) general partnership, |

||||

915 SW Harrison St. |

||||

limited partnership, corporation that has in effect a valid election |

||||

Topeka, KS |

||||

to be taxed as an S corporation under the United States Internal |

||||

Phone: (785) |

||||

Revenue Code, or a limited liability company that has elected to |

||||

Fax: (785) |

||||

be taxed as a partnership under the United States Internal Revenue |

||||

|

|

|||

Code; and, b) that was established and is operated for the sole |

Additional copies of this credit schedule and other tax forms |

|||

purpose of making investments in other entities. |

are available from our web site at: ksrevenue.org |

|||

| Fact Name | Description |

|---|---|

| Governing Law | The Kansas Angel Investor Credit is governed by K.S.A. 74-8133. |

| Qualified Investment Limitations | No tax credits shall be allowed for more than $50,000 for a single Kansas business or a total of $250,000 in tax credits for a single year per investor, who is a natural person or owner of a permitted entity investor. |

| Total Tax Credit Cap | The total amount of tax credits shall not exceed $6,000,000 for each fiscal year from 2011 onwards, except for 2011 when the cap is set at $5,000,000. |

| Credit Transferability | Subject to certain restrictions, this credit may be transferred to another taxpayer, with required documentation of the approved transfer be retained with records. |

Filling out the Kansas K-30 form (Rev. 8/11) is an essential step for angel investors seeking credit for investments in qualified Kansas businesses. This guide simplifies the process, outlining each step to ensure accurate completion of the form. After filling it out, keeping a copy of the approved KTEC certification form with your records is important, alongside documentation of any approved credit transfers. Remember, the Kansas Department of Revenue may request additional information, so maintaining thorough and organized records is crucial.

Once you've completed the form, remember not to send any enclosures with this schedule. Keep a copy of the approved KTEC certification form and any documentation of the approved transfer with your records. Organizing your documents well will streamline the process and help ensure all requirements are met for claiming your angel investor credit.

What is the Kansas K-30 Angel Investor Credit?

The Kansas K-30 Angel Investor Credit is a tax incentive designed for angel investors who provide financial backing to qualified Kansas businesses. By investing in these businesses, investors can receive a tax credit against their income or premium tax. The credit equals 50% of the cash investment made into eligible securities of a qualified business, subject to certain caps: no more than $50,000 for a single business or $250,000 in total credits for a single investor per year.

Who qualifies as an angel investor under the K-30 form?

An angel investor, under the K-30 form, is defined as an accredited investor who is either a natural person or an owner of a permitted entity investor. Such individuals or entities should have a high net worth, as defined by federal regulations, and typically seek high returns through private investments in startup companies. They may also desire an active involvement in the business, offering consulting and mentoring to the entrepreneur.

Can the K-30 tax credit be transferred to another taxpayer?

Yes, subject to certain restrictions, the K-30 tax credit may be transferred to another taxpayer. This provides flexibility for investors to manage their tax liabilities more efficiently. If you have obtained this credit and are considering a transfer, it's essential to retain documentation of the approved transfer as instructed by the Kansas Department of Revenue (KDOR). For more details on the transfer process, investors are encouraged to reach out directly to KDOR.

How is the credit calculated and claimed on the Kansas K-30 form?

To calculate the credit on the Kansas K-30 form, investors must first indicate the total cash investment made in the qualified Kansas business during the tax year. The maximum allowable credit is determined by multiplying this investment amount by 50%. If the investor is part of a partnership, S corporation, LLC, or LLP, they'll also need to calculate their proportionate share of the credit. The total credit claimed in a tax year includes both the current year's investment credit and any carryforward amounts from prior years' Schedule K-30 forms.

Are there any limitations to the K-30 tax credit?

Yes, there are several limitations to the K-30 tax credit. Individual investors can claim no more than $250,000 in total credits per year, and no more than $50,000 for a single qualified Kansas business. Additionally, the cumulative amount of tax credits available statewide is capped annually, with specific limits set for each tax year. It's also worth noting that no tax credits will be available for investments made after the year 2016, and certain types of investments, such as those in Kansas Venture Capital, Inc., are not eligible for the credit.

Failing to accurately record the date the investment was made can lead to processing delays or inaccuracies in credit calculation. The date format mm/dd/yyyy is mandatory for consistency and clarity.

Not specifying the correct name of the qualified Kansas business. It's critical to ensure the business name is exactly as it appears in official records to avoid confusion or misidentification.

Omitting the Employer Identification Number (EIN) of the qualified Kansas business. This particular omission can halt the entire process, as the EIN is crucial for identifying and verifying the business in question.

Overlooking the checkbox for credit transfers can lead to misrepresentation of the credit's origin. This checkbox plays a vital role in tracking the flow of tax credits between entities.

Failing to provide the original investor's complete details, including name, address, and Social Security Number (SSN). This information is essential for the validation and transfer of credits.

Incorrectly calculating the investment amount or the credit. Mathematical errors in these sections can significantly impact the tax credit's value and eligibility.

Neglecting to report the correct carry forward amounts from previous years. Accurately carrying forward unused credits ensures taxpayers maximize their potential benefits.

Miscalculating the Kansas tax liability after all credits other than the one for the current investment year. Accurate calculation is key to determining the allowable credit for the tax year.

Improperly calculating the carry forward credit to the next year can result in either losing out on usable credits or inadvertently claiming more than is allowed, leading to potential audits or penalties.

Each of these errors impacts the accuracy and legitimacy of the K-30 filing. It's vital for individuals to review their entries carefully, double-check their calculations, and ensure that all necessary documentation is in order. Proper preparation and attention to detail can significantly smooth the submission process and enhance the likelihood of receiving the intended tax benefits.

When preparing to file the Kansas K-30 form, which is associated with the Angel Investor Credit, taxpayers often need to gather and complete additional forms and documents to ensure their filing is comprehensive and accurate. These documents provide necessary supplemental information, link the angel investment to specifics about the qualifying Kansas business, and ensure compliance with tax laws. Below is a list of five commonly used documents in conjunction with the Kansas K-30 form.

Together with the Kansas K-30 form, these documents serve to substantiate the claim for the Angel Investor Credit, align investments with qualifying Kansas businesses, and facilitate compliance with state tax requirements. Each document plays a critical role in the process, from proving eligibility to detailing the investment's specifics and calculating the resultant tax credit.

The Kansas K-30 form, known formally as the "Angel Investor Credit," is particularly structured to incentivize investments in qualified Kansas businesses by offering tax credits. This document bears resemblance to other tax incentive forms designed to stimulate economic growth through private investment in specific sectors or regions. By providing a mechanism for tax relief proportional to the amount invested, the K-30 form facilitates a dynamic where both the investor and the qualifying Kansas businesses benefit from enhanced financial support.

One document similar to the Kansas K-30 form is the Federal Form 8941, "Credit for Small Employer Health Insurance Premiums". Both forms are designed to provide tax credits, albeit for different purposes. Form 8941 is aimed at encouraging small businesses to offer health insurance benefits to their employees. Like the K-30, it calculates the credit based on specific expenditures - in this case, premiums paid on health insurance. Both documents share a structured approach to calculating the credit, requiring detailed financial information and adherence to specific eligibility criteria to determine the credit amount. This similarity underlines the broader policy aim of using the tax code to incentivize certain economic behaviors.

Another document that parallels the Kansas K-30 form is the New Markets Tax Credit (NMTC) allocation application. Although not a one-to-one form like K-30, the NMTC process involves a complicated application system where entities specify their investments in low-income communities for tax credit eligibility. Similar to the K-30's goal of spurring economic growth through investments in qualified Kansas businesses, the NMTC aims to stimulate economic and community development in areas that traditionally lack access to investment. Both require applicants to demonstrate their contributions toward specific goals and provide a detailed account of the investment, emphasizing their role in fostering economic development.

Lastly, the California Form 3523, "Research Credit", shares similarities with Kansas's K-30 form in its function as a tax credit incentive, specifically for research and development activities within the state of California. Each form targets a specific type of investment - the K-30 focuses on angel investments in Kansas businesses, while Form 3523 incentivizes investment in innovation. Despite these differences in focus, both forms operate under the principle of using tax credits to encourage private sector investment in key areas, underscoring the versatility of tax credits as tools for economic policy.

When filling out the Kansas K-30 form, a careful approach is required to ensure all details are accurately represented. Below are essential dos and don'ts to guide individuals through this process.

Do:Understanding the Kansas K-30 form, specifically the Angel Investor Credit, can often lead to confusion due to misconceptions about its purpose and utilization. Shedding light on these misconceptions can enable investors and businesses alike to better navigate their tax planning strategies.

Dispelling these misconceptions can help taxpayers navigate the complexities of the Angel Investor Credit on the Kansas K-30 form, ensuring they maximize their benefits while complying with state regulations. Proper understanding and utilization of such credits can significantly impact investment strategies and economic growth within Kansas.

When working with the Kansas K-30 form, several key takeaways are important to keep in mind to ensure the process is both efficient and adheres to the necessary legal requirements. These takeaways offer a clear pathway for investors seeking to utilize the Angel Investor Credit in Kansas.

Understanding these key points will assist taxpayers in accurately applying for and benefiting from the Angel Investor Credit as intended by the Kansas state government. Correct and careful completion of the Kansas K-30 form is integral to securing this valuable tax incentive.

Kdhe Daycare - It requires a physician’s certification if a child is exempt from immunizations due to potential risk to their health.

Kansas Escort Certification - Apply for your Kansas Escort Certification easily with this comprehensive form tailored for new or recertifying escort drivers.

Favn Test - It includes sections for detailed information about the animal, the owner, and the veterinarian submitting the sample.